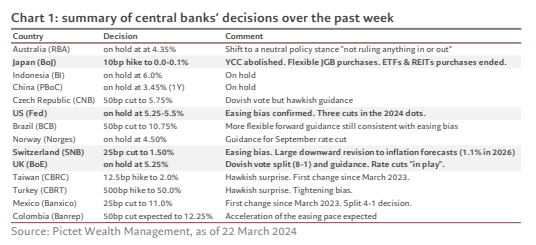

Most central banks confirmed their easing bias.

By Frederik Ducrozet, Head of Macroeconomic Research at Pictet Wealth Management.

- Most developed central banks unambiguously confirmed their easing bias this week. The Swiss National Bank became the first to deliver a 25bp cut in this cycle. Against trend, the Bank of Japan hiked rates for the first time since 2007.

- We continue to expect the Federal Reserve, the European Central Bank and the Bank of England to start cutting rates in June. More importantly, the debate has started over the pace and extent of the easing cycle.

- The US economy stands out as the outlier in terms of labour market resilience and stickier inflation, raising the risk that the Fed does not deliver the five cuts we forecast for this year. However, we believe that a further normalisation of inflation to an acceptable level of “two point something” would be enough for the Fed to start dialling back policy tightening in June.

- Central bankers could now target a more neutral stance so as not to ease too much and risk a resurgence of inflation. But the neutral rate is an elusive concept and almost impossible to estimate in real time. Moreover, the new macro environment facing central banks will likely be characterised by the prominence of supply shocks as well as fiscal and geopolitical risks, resulting in greater uncertainty and macroeconomic volatility.

CENTRAL BANKS TRY DIFFERENT DANCE STEPS , BUT EASING BIAS DOMINATES

A busy week for central banks saw asymmetrical moves in monetary policy. Along- side rate rises in Japan and Turkey, the Swiss National Bank was the first major cen- tral bank in developed markets to cut rates in this cycle. While keeping the excep- tions of Japan and Turkey in mind, we see growing evidence that major central banks are on track to embark on a global easing cycle by the summer. We sum- marise their recent decisions in the table below.

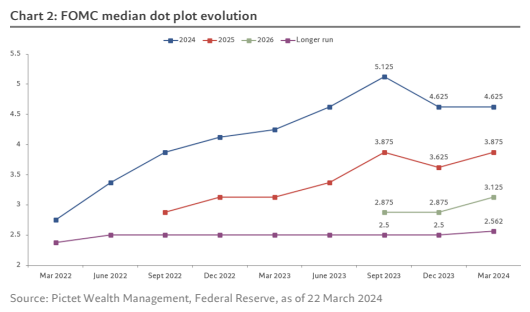

The Federal Reserve (Fed) left the fed funds rate unchanged this week but reaf- firmed its easing bias. The Federal Open Market Committee (FOMC) boosted its growth and inflation projections but, crucially, the median ‘dot plot’ for 2024 stayed at three rate cuts for this year. The margin was thin, with 10 FOMC mem- bers forecast three cuts or more (vs.11 last time), and nine forecasting two or less. For 2024, the FOMC forecasts significantly higher GDP growth (2.1%, up from 0.7%, mostly due to an expansion of labour supply, including immigration) and slightly higher core inflation (2.6%, up from 2.4%).

Importantly, the median dots for 2025 and 2026 were each revised 25bp higher, to 3.875% and 3.125%, respectively, consistent with three cuts each year. The longer-run median moved slightly higher, to 2.6% from 2.5%, suggesting that the FOMC is slowly coming around to the view that the neutral rate is likely higher.

Fed chairman Jerome Powell repeated his previous comment that a rate cut would likely be appropriate at some point this year, with two more consumer price index (CPI) reports before the June Fed meeting carrying significant importance. Powell said the strong inflation numbers in January and February had not changed the broader path of gradual disinflation on a sometimes-bumpy road toward 2%, stress- ing the role of seasonal factors in the numbers.

The risks to our Fed call of a first cut in June and 125bp of cumulative easing are tilted towards a later start and fewer cuts, yet we believe that the Fed’s reaction function remains consistent with a cautious easing cycle starting by the summer. Looking ahead, we have a less constructive view than the Fed on growth and the la- bour market. Powell mentioned at multiple points the risk of employment unex- pectedly weakening, a risk the committee is very much sensitive to.

Finally, Powell noted that the tapering of quantitative tightening (QT) is coming “fairly soon”. We expect QT tapering to be announced in May, with the FOMC tar- geting a gradual approach to the ultimate balance sheet level, i.e. slower for longer.

In Canada, the surprise decline in CPI inflation in February to 2.8% (vs. a consensus expectation for a rise to 3.1%) has fuelled speculation of an earlier-than-expected rate cut from the Bank of Canada (BoC) from the current level of 5%.

The Reserve Bank of Australia (RBA) left its cash rate target unchanged at 4.35% this week but dropped its tightening bias. The March statement noted that “the Board is not ruling anything in or out”, consistent with a neutral stance. RBA gover- nor Michele Bullock justified the communication change as a response to some data that made them “more confident about the path [they] we are on”.