China’s economy and equity markets haven’t had an easy ride. But we believe there are still plenty of attractive investment opportunities – if you know where to look.

James Kenney, Senior Investment Manager, Pictet Asset Management.

Investors in Chinese equities have had a tough couple of years, a period marked by disappointing economic growth, regulatory crackdowns on a number of industries and ongoing tensions between Washington and Beijing. Many of these clouds have yet to dissipate.

A weak property market will continue to drag on growth, deflationary pressures could linger, and exports will stagnate. The infrastructure investment cycle, which had held up because of significant investment into renewables and clean energy, is also likely to moderate given the exponential increases in capacity over the past 24 months. At the same time, workers are still feeling the impact of 20-30 per cent wage cuts by state-owned enterprises.

Without policy support, it hard to see any improvement.

Fortunately, there is some good news on this front. The authorities have cut the reserve requirement ratio (RRR) and interest rates, and are offering financial support to property sectors, loosening home purchase restrictions (HPR) and encouraging investment into key sectors such as technology and automation.

While this may not be enough to immediately turn around the economy, such measures lay the foundations for a sustainable recovery. They are deliberately modest to avoid exacerbating other problems including high debt leverage and the dominance of property investment.

More support is expected over the coming year, particularly if the US Federal Reserve also eases policy as is widely expected. Fed cuts will leave China more room to lower its own rates without the risk of provoking capital outflows and causing further currency weakness.

Our economists see China delivering GDP growth at an above-consensus 4.8 per cent this year, broadly in line with potential and nearly five times the pace expected for developed economies.

All about balance

So where does that leave Chinese equities? Economic growth of this magnitude might not fuel a powerful rally in stocks, but it won’t be a drag on the market either.

We take nuanced view. There is no escaping the fact that stock market liquidity is thin. Share price swings have become more violent than before. Video game firms Netease and Tencent,1 for example, dropped by 25 per cent and 12 per cent respectively in just one day in December on news of possible regulatory tightening in the sector. However, we don’t agree with those who argue that China is un-investable. Despite the online gaming blip, the overall direction for regulation seems to be easing, with the government becoming more supportive of businesses and advocating a stable and friendly policy environment.

What is more, valuations are very compelling – models devised by our multi asset strategies show that Chinese stocks are the cheapest they’ve ever been in the past 20 years and cheaper than any other major equity market. That in itself, of course, is not a reason to buy, but it does create attractive entry points for areas of the market where future prospects look strong.

The actions of foreign investors also suggest the market may be due a bounce. In 2023, foreign entities cut their holdings of Chinese equities by 13 per cent according to data from the Peoples Bank of China, building on withdrawals in the preceding two years. This leaves plenty of scope for a turnaround and latest numbers from other sources suggest that may now be starting to happen. Since the start of the year, Chinese equities have seen USD50 billion of flows, according to EPFR data, and purchases by foreign investors have overtaken sales in recent weeks, according to Bloomberg.

The key for equity investors in China is to be selective, both in terms of sectors and individual companies. China is clearly moving away from past economic drivers of property and construction, towards new ones like electric vehicles, industrial automation, AI, technology localisation are key drivers of the economy.

It could take some time for sentiment to turn. And it’s also possible that the market will continue to trade at a sizeable discount to where it has in the past given the structural concerns of slowing growth, policy uncertainty, an aging population and ongoing geopolitical tensions.

Embracing the trend

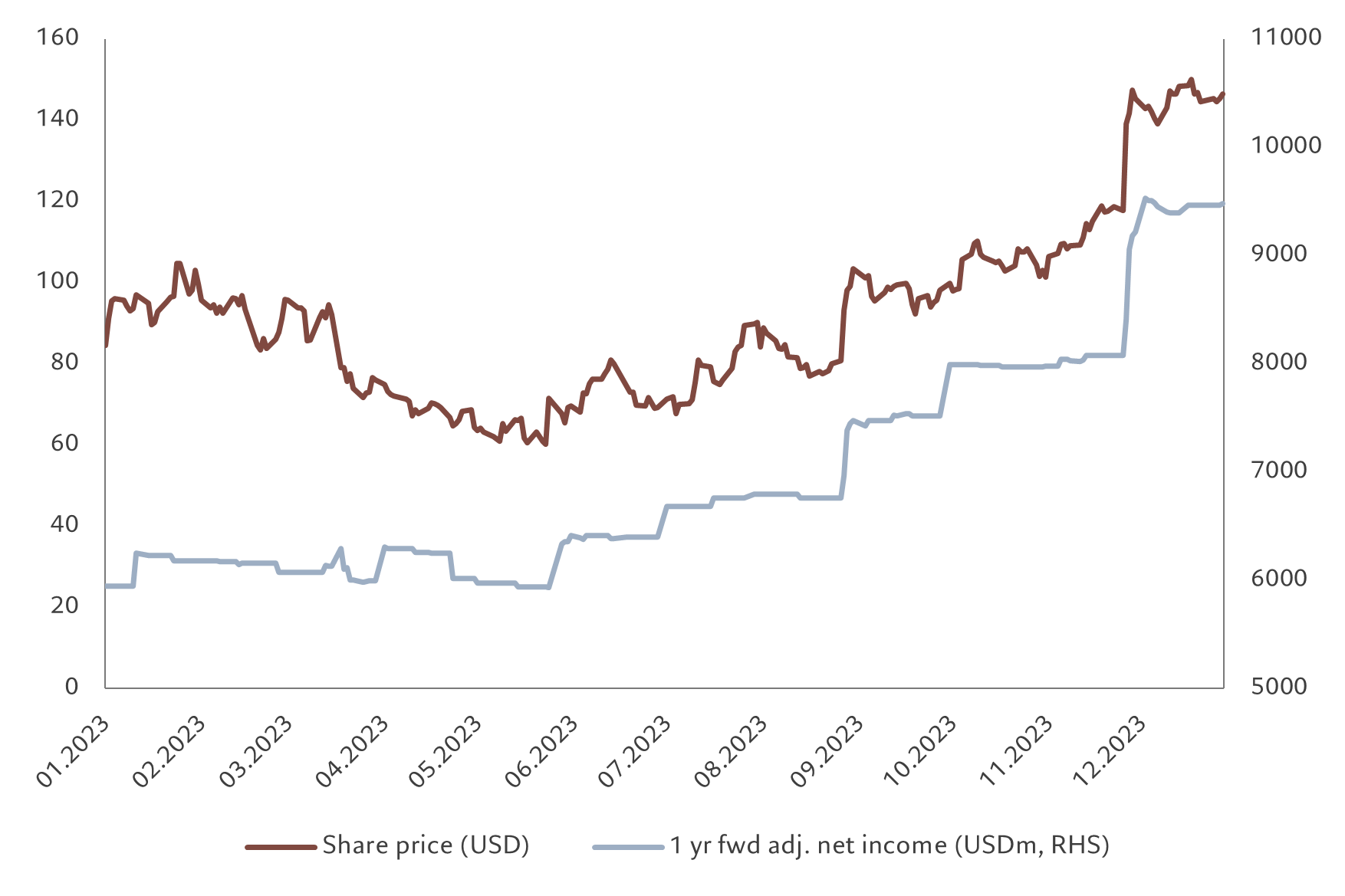

PDD share price and earnings revisions

Source: Bloomberg, Pictet Asset Management. Data from 12.01.2023 to 29.12.2023.

But with literally thousands of listed companies, we remain focused on investing in high quality firms with good growth profiles and attractive valuations.

Despite the challenging nature of the market in 2023, it is encouraging to see that companies with solid medium-term fundamentals are beginning to pull away from those with weaker prospects. At the same time, paying attention to certain trends can offer rewards. Take changing consumption patterns. With consumers gravitating towards buying cheaper goods, for example, discount e-shopping firms such as PDD and Temu are performing well while higher end rivals are struggling (see chart).

The case for diversification

Of course, risks remain, not least geopolitical ones. Taiwan’s recent elections and the prospect of a new Trump presidency in the US are major concerns. Both US presidential candidates are likely to talk tough on China to gain popularity and votes.

In this environment, we want to maintain a diversified portfolio. We see opportunities across two areas in particular. Firstly, long-term structural growth dynamics favour sectors like electric vehicles, industrial automation, artificial intelligence (AI) technology and export-focused industries. In the short-term, of course, they are not immune to swings in supply and demand. We may see weakness in some areas, which makes a selective, top-down approach all the more important. (The consumer sector is a case in point. E-commerce players are facing stiff competition and slowing sales growth, but some companies like PDD have the capacity to buck the broader trend.)

Secondly, there are a number of sectors in which are currently seeing a recovery in demand. In tech, the market for computers and smartphones (and the components that make them) is fuelled by the replacement cycle, restocking and the rise of AI. Other industries are recovering from earlier regulator crackdowns and benefiting from a friendlier policy stance. Education was hit hard by restrictions on after-school tutoring since 2021, but now the situation seems to have stabilised and demand is very strong, boosting companies like New Oriental Education.

While we wait for confirmation of a stabilisation in economic conditions and an easing of geopolitical risks, a degree of caution is warranted. However, we are in no doubt that China is and should remain a strategic element of portfolio allocation. The key is to be selective, maintaining a diversified exposure and a long time horizon, align investments with Beijing’s economic objectives and focus on finding the companies with the strong fundamentals and the potential to become global leaders.

[1] The companies mentioned are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific company or security is not a recommendation to buy or sell that security.