Frederik Ducrozet, Head of Macroeconomic Research, chez Pictet Wealth Management.

The ECB is all but certain to hike its policy rates by 25bp at this week’s meeting of the Governing Council (GC), bringing the deposit rate to 3.50%, while signaling that it might have “more ground to cover”. How strongly the central bank commits to additional rate hikes remains to be seen, however, with some important nuances likely to be added to the forward guidance (or lack thereof).

The ECB has several options here, but the laziest best one may be to leave the second paragraph of the May introductory statement unchanged, stressing the ECB’s goal to bring back inflation to 2% in a timely manner without pre-committing to any specific rate path. The ECB has made it abundantly clear that future decisions will be more data dependent as policy rates are getting closer to their peak. In particular, the statement is likely to repeat that “past rate increases are being transmitted forcefully to euro area financing and monetary conditions”.

The risk going into this week’s meeting is skewed towards more hawkish communication but more dovish staff projections, in our view.

We don’t expect the ECB to state its “intention” to hike rates in July, having dropped that kind of wording in March. More likely, President Christine Lagarde may shed some light on the GC discussion and note that on the basis of available data, and/or unless inflation data improve more convincingly in coming months, a majority of members would be in favour of hiking rates again in July.

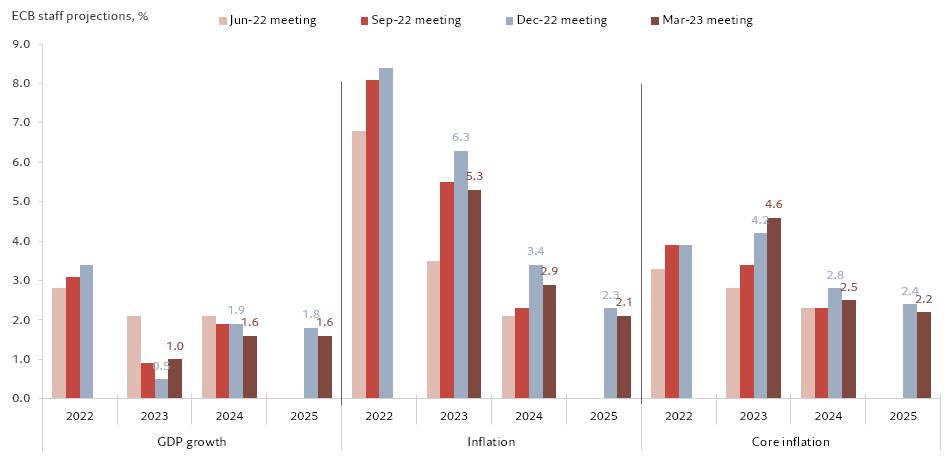

The downward revision to euro area GDP, pushing the region into a technical recession, was led by volatile data in Germany, the Netherlands and Ireland. This may drive a small downward revision to ECB staff projections for growth, but the bigger picture remains unchanged. The euro area has proved to be much more resilient than expected to an unprecedented combination of shocks to real incomes. Crucially, as long as unemployment remains close to cyclical lows, the ECB is very unlikely to reverse course.

The ECB’s biggest concern remains price stability. The most recent data have been consistent with our view that core inflation dynamics have turned, but the disinflation process is likely to be unusually slow and bumpy. Lagarde noted in a recent speech that “there is no clear evidence that underlying inflation has peaked” as “wage pressures are becoming a more important driver of inflation”, echoing similar comments from Executive Board member Isabel Schnabel.

We expect the June Staff projections to show some limited progress towards the inflation target. Headline inflation may be revised slightly lower, with the 2025 median projection likely to be lowered to 2% (from 2.1% in March), following four quarters of overshooting the target. Lower energy prices should help, as well as a slightly stronger exchange rate and a wider output gap. However, core inflation is unlikely to be revised lower despite the encouraging print in May, because of stickiness in the prices of services and strong wage pressures.

In all, the ECB will continue to have more questions than answers, fueling disagreements between the hawks and the doves about “the lags and strength of transmission of monetary policy to the real economy”. We still believe that there is a strong case to pause sooner rather than later, but acknowledge that the risk of another rate hike in July remains high. A July hike doesn’t look like a done deal either, if only because of the uncertainty related to the US outlook and the Fed. The ECB may be tempted to ‘skip’ July and to shift to quarterly decisions based on the staff projections going forward.

Away from policy rates, the ECB should confirm that APP reinvestments will be discontinued as of July 2023. A more important talking point will be related to the upcoming repayment of a large tranche of TLTRO loans on 28 June 2023, with €477bn maturing (down from the initial allotment of €1308bn following large voluntary repayments in the last three years). While market participants might be worried about the consequences of this liquidity withdrawal, the ECB is unlikely to budge. Excess liquidity currently stands at €4.2 trillion and while some peripheral banks could face funding pressures as their excess reserves are lower than their TLTRO borrowings, this is likely to remain contained to isolated cases. We don’t expect the ECB to announce new LTRO ‘bridges’ any time soon.

ECB: staff projections