The process of globalisation is unlikely to end completely, but it is facing increasing challenges. In the next decade, we expect trade frictions to continue to lead to higher inflationary pressure and more financial instability.

Nadia Gharbi, Senior economist, Pictet Wealth Management.

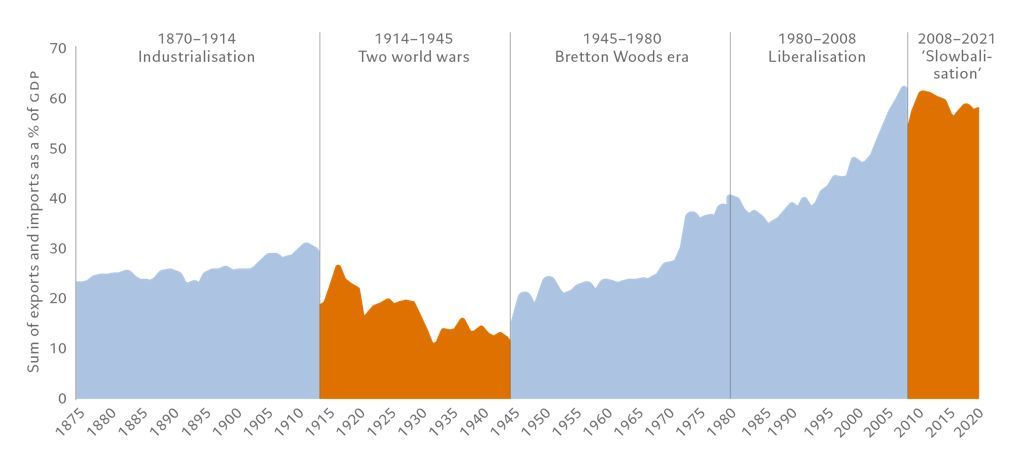

Globalisation, broadly defined as the increasing integration of the global economy through trade, capital and migration flows, has been a significant driver of economic growth for over four decades, particularly for developing economies. But globalisation’s rise has never been a linear process. As the chart below shows, it has progressed in fits and starts since the late 19th century but went into reverse during the two world wars and the Great Depression that started in 1929.

Globalisation really picked up after 1945, and gained a further boost following the collapse of the Soviet Union at the start of the 1990s and China’s accession to the World Trade Organisation in 2001. But growth in the flow of goods has faltered since the global financial crisis (GFC) of 2008–2009, leading to what some observers have labelled ‘slowbalisation’1. Some go further and believe that we have entered an era of ‘deglobalisation’, characterised by a reversal of global integration through trade and the decoupling of trade links between countries in response to geopolitical or domestic imperatives.

Globalisation through recent history

Trade openness metric – the sum of exports and imports of all countries relative to global GDP.

Source: Pictet Wealth Management, Jordà-Schularick-Taylor Macrohistory database; Penn World Data (10.0); Peterson Institute for International Economics; World Bank; International Monetary Fund staff calculations, as of 28.02.2023

Rising discontent with globalisation – stemming in particular from increased inequality, rampant immigration and the loss of manufacturing jobs – has fuelled political populism and trade tensions in recent years. The UK’s vote to leave the EU in 2016 and the emergence of US-China trade tensions since 2018 are examples of the kind of populism and protectionism that have challenged the traditional model of globalisation, reduced its speed and increased policy uncertainty.

More recently, the covid-19 pandemic has put globalisation under further pressure by highlighting the vulnerability of global supply chains and exposing the risks of excessive dependence on a few key players. This has led many countries to rethink the way their economies operate, giving a boost to efforts to shorten and diversify supply chains and reduce reliance on single-source suppliers. The war in Ukraine has also prompted deep reflection within countries about the security of supply chains and dependency on unreliable partners for critical commodities. This has been prompting countries to shift supply chains and production home or to ‘friendly’ countries that share the same values2 as they do. This phenomenon, known as ‘friendshoring’, is evident in areas like oil and gas.

Several inward-looking policies, such as the Biden administration’s Inflation Reduction Act (IRA) in the US, Beijing’s ‘Made in China 2025’ industrial strategy and the EU’s ‘Chips Act’ (designed to reduce European manufacturers’ dependence on US and Asian semiconductor producers), have also emerged in the world’s three major trading blocs in the name of national security and competitiveness, further challenging international cooperation. At the same time, data show that countries are imposing a growing number of trade restrictions, notably in high-tech sectors. Of particular note has been the decision by the Biden administration to restrict US exports of advanced chipmaking equipment to China in an effort to slow the latter’s advances in cutting-edge technology.

While the process of globalisation is unlikely to end completely, it is facing increasing challenges. US-China trade tensions and Russia’s invasion of Ukraine will probably be seen as important markers of a more fragmented world, with important economic consequences over the long run. Notably, the extent to which the US and China try to bind their allies closer and cement influence in different parts of the world will be critical to watch. In technology, the US is increasingly asking its friends to pick their side, stoking further tension with China. Thus, we are probably heading towards a world with more trade frictions.

Globalisation acted as a major driver of deflation in the developed world by reducing production and labour costs. By contrast, the main features of deglobalisation – higher tariffs and a shift from global to regional trade flows – will likely contribute to higher inflationary pressure in the years ahead. For many countries, producing at or closer to home will mean an increase in production costs and, ultimately, in sales prices. Other potential implications could be lower growth and increased risk of financial instability. Simulations carried out by the International Monetary Fund (IMF) showed that a shift towards economic blocs and the imposition of investment and tariff barriers against those outside these blocs would significantly hurt economic efficiency over the long term. The IMF suggested that the cost could be as much as 1.2% of world GDP. The cost rises to 1.5% when non-tariff barriers in other sectors3 are added. Trade-intensive countries in the Asia-Pacific region would be disproportionately affected, losing about 3.3% of GDP in the most severe scenario4.

[1] Aiyar, Shekhar, Ilyina, Anna, and others (2023). Geoeconomic Fragmentation and the Future of Multilateralism. Staff Discussion. Note SDN/2023/001. International Monetary Fund, Washington, DC

[2] Remarks by Secretary of the Treasury Janet L. Yellen on Way Forward for the Global Economy, 13 April, 2022

[3] The analysis considers a scenario in which non-tariff barriers in other sectors are also increased between blocs, in addition to the elimination of trade in the energy and high tech sectors.

[4] International Monetary Fund (IMF). 2022a. Regional Economic Outlook: Asia and Pacific. Washington, DC