What risks for the global economy ?

Bruno Cavalier, Chief Economist ODDO BHF Asset Management.

KEY HIGHLIGHTS:

- The global economy has proven surprisingly resilient to shocks over the past two years.

- Disinflation and lower rates should extend the soft- landing path.

- A deviation from this path remains possible because global growth is poorly distributed.

- A re-election of Trump would have strong disruptive potential for trade and geopolitics.

The global economy has overcome two shocks of rare intensity that could have brought it to its knees. But it didn’t. Firstly, the inflation surge that swept the world in 2021 and 2022 has now largely subsided. According to Bloomberg’s estimate, the global inflation rate, which had soared to over 10% by the end of 2022, is now around 5%. In Europe, inflation has fallen back below 3%, thus edging towards the 2% target. Secondly, the sharp rise in interest rates has also stabilised, as central banks deem their tightening measures sufficient. They are even considering the start of monetary easing in the coming months.

The surge in inflation has undeniably reduced households purchasing power, but not to the point of triggering a recession. While rising interest rates have made financing more expensive, the economy has largely absorbed these restrictive effects with minimal damage, apart from the impact on mortgages. Remarkably, labour markets have remained strong and no sharp rise in unemployment was needed to curb inflation. Looking ahead, the prevailing consensus can be summed up as follows: disinflation will restore consumer confidence and boost consumption, while lower interest rates will alleviate financial pressures on businesses and spur investment. Some would even say we’re standing on the cusp of a productivity boom driven by advancements in artificial intelligence. Isn’t this too good to be true?

Between the Cassandras who constantly predict the imminence of a new crisis and the Panglosses who see the world through rose-tinted glasses, there is room for a reasoned approach to risk. To help with the analysis, let’s distinguish between economic, political, and geopolitical risks, bearing in mind they do interact with each other.

Economic risks – While the global economy has managed to avoid the worst, it is still showing signs of weakness. A primary concern is the growing disparities between major regions. In 2023, the United States experienced GDP growth exceeding its potential, whereas Europe faced stagnation, and China was unable to initiate a lasting recovery despite the easing of health restrictions. This uneven distribution of global growth contributes to its sluggish outlook. According to IMF estimates, global growth is expected to hover around 3% this year, compared to a trend between 3.5% and 4% prior to the pandemic.

Secondly, public finances have worsened. With higher refinancing rates, governments are now forced to closely monitor their debt trajectory. This situation could result in more restrictive fiscal policies, potentially curtailing investment programs crucial for addressing future challenges like defence, technology, and climate change. Here again, the United States stands as an exception, buoyed by the dollar’s dominance, as it continues to run excessive deficits. This, however, risks overheating the economy and, possibly, causing the Federal Reserve to delay interest rate cuts. It would be a major disappointment for financial markets, which have staked so much on this monetary policy pivot.

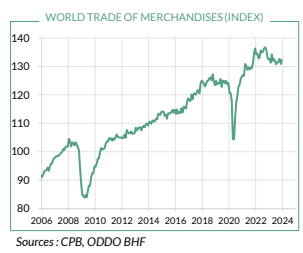

Finally, global trade is becoming increasingly fragmented. Following the financial crisis of 2008 and even more so after the 2020 pandemic, free trade is no longer seen as a virtue benefiting all countries. Protectionist tendencies are emerging worldwide, albeit under different names such as industrial policy, supply chain security, and national independence. As a result, world trade has been sluggish for the past two years (see chart).

Political risks – In 2024, around seventy countries representing roughly half the world’s population will hold elections. Yet, only one has the capacity to send shockwaves across the globe: the US presidential election on November 5th. This election is unusual in many respects. It marks a rematch from 2020 between Joe Biden and Donald Trump, two elderly men whose health, both physical and mental, has been a subject of public concern. As is often the case, the outcome is expected to hinge on a few swing states, decided by a slender margin of a few hundred thousand votes from more than 160 million registered voters. The race is still very much up for grabs.

Donald Trump has never conceded his 2020 election defeat. He is driven by a desire for retribution, especially now that he’s entangled in numerous legal battles. His economic platform mirrors that of 2016 but pushed to further extremes. Economically, he is promising two things: lower taxes for businesses and higher tariffs. Dubbing himself “Tariff Man” in 2016, his primary focus was on China. This time around, he aims to impose taxes on all imports, regardless of their origin, potentially provoking retaliatory measures from other nations. Internationally, Trump vows to scale back the United States’ longstanding alliances with Europe and Asia, introducing greater unpredictability into global affairs.

Geopolitical Risks – The main global hotspots—Asia, Ukraine, and the Middle East—each carry the risk of escalation, owing to the intricate nature of their respective conflicts. Asia represents the primary battleground for the strategic rivalry between the United States and China. Although a direct conflict between these two technological and military contenders is thankfully not on the table, underlying tensions persist, likely influencing economic conditions. In Ukraine, more than two years of conflict have led to a growing sense of fatigue among Western observers, with leaders caught between refusing Russia a decisive advantage and reckoning with the cost implications of a deeper commitment to Ukraine. The mention of nuclear risks by figures on both sides highlights the extraordinary level of uncertainty of this conflict. In the Middle East, a critical hub for oil and gas, history has shown the potential for wars to significantly impact energy markets and the broader economy. While regional powers have so far sidestepped such outcomes, trade flows typically navigating the Suez Canal have been diverted around Africa. The resulting disruptions and additional costs may not match the scale of those experienced during the pandemic, but they contribute to the ongoing fragmentation of the global landscape.