Long-term investors should not fear the US election

Prof. Dr. Jan Viebig Global Co-CIO, ODDO BHF AM.

“Investors with a long-term perspective, such as a ten-year horizon, can afford to be somewhat relaxed about the impact of the US election on their assets.”

The outcome of this year’s US presidential election may have far-reaching consequences in many areas. However, we believe that the impact on the financial markets will be limited for long-term investors, as we consider ourselves to be. Over an extended period of time, there are other forces at play. Investors with a long-term perspective, such as a ten-year horizon, can afford to be somewhat relaxed about the impact of the US election on their assets.

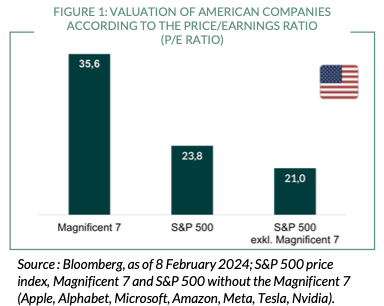

In recent months, investors have focused heavily on the ‘Magnificent Seven’, comprising big tech stocks Meta, Amazon, Google, Microsoft and Apple alongside electric car manufacturer Tesla and semiconductor producer Nvidia. These companies have dominated the US stock market over the past year, resulting in today’s high valuations – in our view, some of the ‘Magnificent Seven’ are even overvalued. As Figure 1 shows, the ‘Magnificent Seven’ have an aggregate price/earnings ratio (P/E ratio) of an impressive 35.6, while the valuation of the other 493 stocks in the S&P 500 is close to their long-term averages, with the S&P 500 currently trading at a P/E ratio of 23.8.

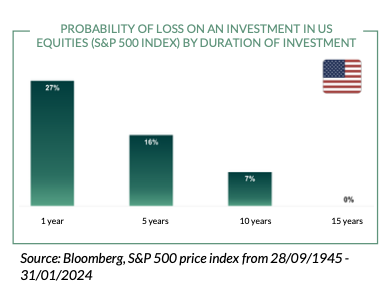

Those investing in equities should have a long-term investment horizon. In our opinion, short-term equity investments in particular harbour a high level of risk. Indeed, Figure 2 shows that over a one- year investment horizon, the probability of suffering a loss on the US stock market was 27 %. This risk fell to 16 % if investors remained invested for five years, and to 7 % for a ten-year investment period.

Anyone who opted for American equities for at least 15 years never suffered a loss in the period shown below. While past performance is not indicative of future outcomes, they underscore a clear trend: the longer the investment duration, the lower the risk of loss with US equities.

The worst one-year period on the US stock market occurred during the financial crisis, from 28 February 2008 to 28 February 2009, during which a 44.8 % decline in prices was recorded. The best one-year period happened during the Covid crisis from 31 March 2020 to 31 March 2021, with a price gain of 53.7%.

These figures are calculated on a nominal basis before inflation. However, inflation can significantly reduce the purchasing power of an asset, especially over long periods of time. It is inherently risky to draw conclusions about the future from extensive historical trends. Yet, this approach remains a standard practice among statisticians.

From 1900 to 2022, US equities rose by an average of 6.4% (geometric mean) or 8.3% (arithmetic mean) in real terms, i.e. after adjusting for inflation. Researchers Dimson / Marsh / Staunton (2023) concluded that the US stock market was the most successful among 21 countries over this extensive timeline, in real terms.

In addition, the volatility of US equities during this 123- year period was lower than that of both German and French stocks: at 19.9% p.a., the standard deviation of the real returns of American equities was lower than the average standard deviation of German equities of 31.1% p.a. and French equities of 22.8% p.a.*

Timing becomes less relevant as the investment period increases: the necessity to purchase shares at their lowest and sell at their peak becomes less critical. Neither is usually possible anyway, and when it does happen, it’s often a matter of luck. Ultimately, the biggest mistake is to believe that one can predict a stock’s performance over a period of three weeks or even three months.

There are several reasons for the positive long-term performance of US equities. A culture of growth and innovation as well as the high level of transparency and accessibility of the US equity markets make investing in US stocks appealing. The American economy is also one of the most innovative in the world, particularly evident in the technology sector. This capability extends beyond technology to many other industries such as healthcare, where digitalisation and MedTech are playing an increasingly important role. Technology, including artificial intelligence, is transforming entire industries, from education to transport and retail, among others.

Furthermore, the US is a huge domestic market where companies that succeed achieve a large sales volume and are well positioned to be successful globally. These factors make a compelling case for long-term investment in American shares, particularly in “great stocks”: companies with high returns on capital, clear competitive advantages, structural growth, fair valuation, and good governance.

The innovative and growth capabilities of the American economy also translate into high profitability. Since 1999, according to MSCI index data, the return on equity of American stocks has beaten that of European equities by more than 3 percentage points p.a., averaging almost a 14 per cent return. Most recently, the lead has increased to 5 percentage points. This is a key reason why US stock markets are outperforming their European counterparts.

* Note: The “Investment Returns Yearbook” by Elroy Dimson, Paul Marsh and Mike Staunton is published annually. The latest figures relate to the period 1900 to 2022.

{kind=link}