France-Germany, the sick couple of Europe

Bruno Cavalier, Chief Economist ODDO BHF Asset Management.

KEY HIGHLIGHTS:

- The European economy has been stagnant for nearly two years.

- The growth outlook for 2024 is gloomy, especially in Germany and France.

- The Franco-German partnership has weakened, both politically and economically.

- The fall in energy prices and a possible cut in ECB interest rates should revive the economy.

When a European country is in particularly bad shape, it is common for observers to refer to it as the “sick man of Europe”, followed by the “new sick man of Europe”, and so on. Every country has borne this infamous title at one time or another. In the 1960s and 1970s, it was often the United Kingdom. In the 1990s, it was Germany, as it bore the costs of reunification. All the peripheral countries that suffered debt crises between 2010 and 2015 were also eligible. To vary the expression, German journalists at the time had coined a new word for France: Krankreich, a contraction of krank (sick) and Frankreich (France).

What about in 2024? Who is the “new sick man of Europe”? One might be tempted to answer “Europe” as a whole, given its recent mediocre economic performance. The general deterioration in the social climate is clear proof of this. By the end of the Great Lockdown in mid-2020, a strong recovery had taken over, giving good hope of a lasting upturn. Unfortunately, the war in Ukraine and the energy crisis, followed by the sharp monetary policy tightening, put an end to this momentum. Worse still, these events revealed deep-seated weaknesses, so much so that the end of these shocks (end of rate hikes, fall in energy prices) does not guarantee the economy will suddenly take off again.

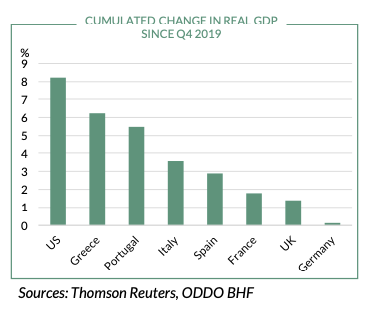

Here are a few figures to put things into perspective. Real GDP in the eurozone has not grown at all since mid-2022, meaning six quarters of stagnation. In a normal trend growth scenario, activity would have grown by 2.5% over this period. By comparison, real GDP in the United States rose by 3.8%. In terms of growth expectation, recent IMF and OECD reports forecast European growth of just over 0.5% in 2024, compared with 2% on the other side of the Atlantic. For once, in recent years, the countries of southern Europe have been much more dynamic than the heart of the zone. Germany is at the back of the pack (chart). France is not doing much better. Rather than a sick man, we should be talking about a “sick couple”.

What are the causes of this malaise? Some of them affect all countries to varying degrees, while others are specific to each individual case. The inflation shock is a common factor that has reduced purchasing power, and consequently curbed domestic demand. However, the surge in prices has been fairly similar in the major developed countries and cannot explain the differences in performance. Monetary tightening is another common shock, but in that respect the sensitivity of each country has varied depending on the transmission to the construction sector.

After the sovereign debt crisis, peripheral countries were forced to shrink their bank balance sheets. As a result, there was no credit boom during the 2015- 2021 period of ultra-low interest rates. According to estimates by the Banque de France, mortgage origination in Italy and Spain was around €60 billion a year by 2021, but four times as much in France and Germany. Consequently, when the flow of credit dried up, the impact was felt harder in countries where the construction sector was booming at the time.

Turning now to the specific factors. For nearly two decades, the German economy could be described as a great industrial power that had taken advantage of globalisation (the rise of China) and monetary integration (a competitive exchange rate) to generate substantial external surpluses and persistent budget surpluses. This ‘model’ has reached its limits. The reality is now different. China is no longer just an export market but a major competitor. The industry must deal with rising wage costs and a new energy situation. Production in the most energy-intensive sectors (chemicals, metallurgy) has fallen by almost a quarter since the war in Ukraine. The entire ecosystem of the automotive sector, whose excellence was recognised worldwide, has been turned upside down by the transition to electric vehicles. The government budget has been in deficit since 2020. The ‘debt brake’ rule is even being openly criticised by some for being too rigid.

The French ‘model’, if it exists, is harder to describe, but one of its weaknesses is undoubtedly the weight and inefficiency of public spending. This was true before the pandemic. It has worsened since. The measures taken to overcome the Covid crisis, followed by those designed to cushion the energy crisis, have planted the idea in people’s minds that the only answer to every problem is more government spending. Public investment, which could be expected to have a positive effect on growth potential, has been relegated to second place. Since 2019, it has risen by 23% in France, 29% in Germany, and more than 40% in Italy and Spain.

It’s not always easy to distinguish between cyclical difficulties and structural hindrances (demographics, productivity). The two are undoubtedly intertwined in the current situation. The now well-advanced decline in inflation, the normalisation of energy prices and, in a few months’ time, a probable easing of the ECB’s monetary policy should provide some relief to the “sick couple” of Europe.